Remember that feeling when you first started earning? The pride, the freedom, the endless possibilities? Buying your first home brings back that exact rush—only magnified. But let’s be honest, it also brings a fair share of anxiety. Will I choose the right location? Am I paying too much? What if I miss something important?

If you’re reading this with a knot in your stomach, take a breath. You’re not alone, and more importantly, you’re already doing the right thing by seeking information before diving in.

Understanding What You Really Need (Not What Instagram Says You Need)

Before you fall in love with that stunning duplex your colleague just bought, pause. Your first home should match your life, not your aspirations for someone else’s life.

Ask yourself these honest questions:

- How long is your daily commute, and can you handle adding another hour to it?

- Are you planning to start a family soon, or is it just you (and maybe a plant you're trying to keep alive)?

- Do you actually need that extra bedroom, or would you rather have money left for, you know, furniture?

For instance, if you’re working in Whitefield’s tech corridor, a 2 BHK near your office—with good connectivity and established infrastructure—might serve you better than a sprawling 3 BHK in a far-flung locality. It’s not about compromising; it’s about being smart with your first investment.

Location: The One Thing You Absolutely Cannot Change

You can renovate a kitchen. You can repaint walls. You cannot pick up your building and move it closer to your office or your aging parents.

Here's what actually matters:

- Can you reach a decent hospital in under 20 minutes? (Trust me, this matters more than the gym in the clubhouse)

- Are there actual, functioning schools nearby if you have or plan to have kids?

- Is the area developing, or has it already developed and stabilized?

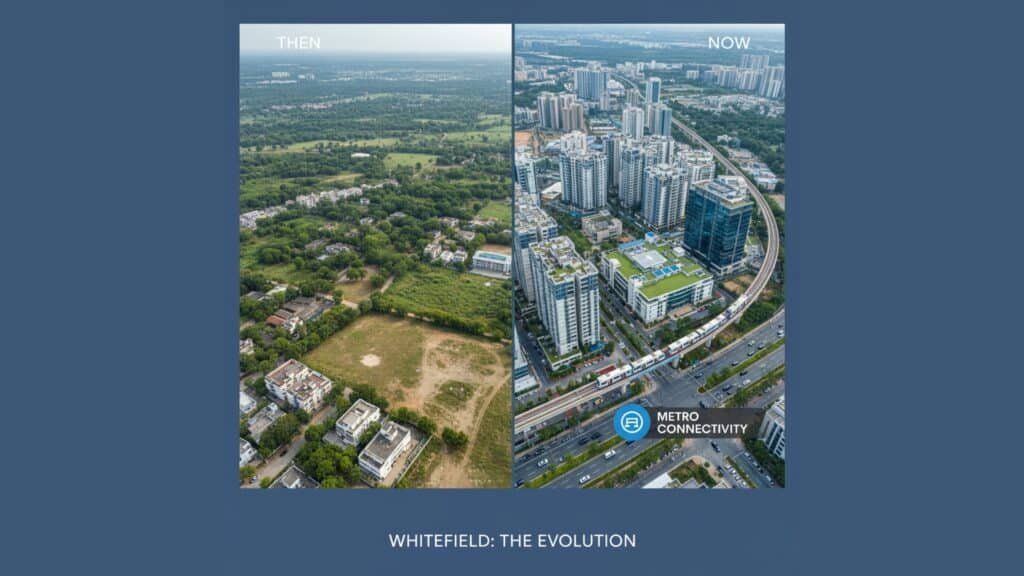

East Bangalore localities like Whitefield, Hoskote, and Kadugodi have seen tremendous infrastructure growth over the past few years. The Peripheral Ring Road, improved metro connectivity, and the concentration of IT companies have transformed these areas from “upcoming” to “arrived.” But within these localities, the micro-location still matters—proximity to main roads, noise levels, and neighborhood safety are non-negotiable.

For first-time buyers, Whitefield presents an interesting case study. Yes, it’s more expensive than outer areas, but the infrastructure is already in place. You’re not betting on future development—you’re buying into existing convenience. Areas like Nallurahalli, for instance, have become particularly attractive because they offer the Whitefield advantage (proximity to tech parks, hospitals, schools) without being right in the chaotic center.

The Money Talk: Beyond the Brochure Price

That attractive price you saw advertised? It’s probably just the apartment cost. The actual money you’ll need is more like a layered cake with several expensive layers.

Budget for these reality checks:

- Registration and stamp duty (around 7-8% in Karnataka—yes, really)

- Home loan processing fees and insurance

- Interior work (because those bare walls won't decorate themselves)

- Maintenance deposits and initial setup costs

- A 6-month emergency fund (because water heaters break at the worst times)

Financial advisors typically recommend that your EMI shouldn’t exceed 40% of your monthly income. If you’re stretching beyond that, you’re not buying a home; you’re buying stress.

This is where configuration flexibility becomes crucial. Maybe you love the location but a 3 BHK pushes your budget uncomfortably. Would a 2.5 BHK work? It’s essentially a 2 BHK with a smaller third room—perfect as a home office or nursery—without the full financial commitment of a standard 3 BHK. Not all projects offer this configuration, but when they do, it’s worth serious consideration for first-time buyers who need that middle ground.

Home Loan Decoded: What Banks Won't Clearly Tell You

Getting a home loan approved isn’t the same as getting a good home loan. Interest rates vary, and even a 0.25% difference means lakhs over 20 years.

Pro moves for first-time borrowers:

- Check your credit score before applying (above 750 gets you better rates)

- Apply for pre-approval to understand your actual budget

- Compare offers from at least three banks (yes, it's tedious, but so is paying extra for 20 years)

- Understand the difference between fixed and floating rates

- Factor in processing fees, which can run up to 1% of the loan amount

Also, here’s something most people miss: If your property is in an established project with good builder credentials and proper RERA registration, banks are more confident about approving loans quickly and at better rates.

New Project vs. Ready-to-Move: The Great Debate

Getting a home loan approved isn’t the same as getting a good home loan. Interest rates vary, and even a 0.25% difference means lakhs over 20 years.

Choose under-construction if:

- You have time on your side (2-3 years before you need to move in)

- You want to save 10-20% on costs

- You're okay with some uncertainty around timelines

- You can continue renting comfortably

Go for ready-to-move if:

- You're done with landlords and want your keys now

- You need certainty and want to see exactly what you're buying

- You can manage the higher initial cost

- You're currently paying high rent that could go toward an EMI

Here’s a real scenario: You’re a couple working in Whitefield, planning to start a family in two years. A 2 BHK feels tight for the future, but a 3 BHK stretches your budget uncomfortably. This is exactly where a 2.5 BHK configuration becomes your perfect fit—think of it as a 2 BHK that grows with you.

Instead of struggling to shortlist projects or decode market jargon, first-time buyers can benefit from Diligent Enterprises’ Real Estate Consulting Services. Their team offers comprehensive real estate guidance—from identifying the right property and evaluating micro-locations to assisting with home loans, RERA verification, and interior design.

With Diligent’s expertise, you gain access to data-driven project comparisons, transparent advisory, and personalized support—ensuring that your first home fits both your lifestyle and your financial goals. Whether it’s a 2 BHK near your workplace or a future-ready 2.5 BHK that balances comfort and affordability, Diligent helps you make a confident, well-informed decision.

The Visit: What to Actually Check

When you visit a property, you’re not there to admire the model apartment’s expensive furniture. You’re there to investigate.

Your inspection checklist:

- Water pressure in bathrooms (turn on all taps simultaneously)

- Mobile network strength (actually make a call)

- Natural light and ventilation (visit during daytime)

- Sound insulation between units (if you can)

- The actual view from the apartment (not the brochure photo)

- Common areas maintenance (are they actually maintained?)

- Talk to existing residents if it's a ready property (they'll tell you the real story)

Don’t be shy about asking questions. The sales person might sigh, but you’re the one who’ll be living there. Ask about water supply timings, power backup capacity, and pest control frequency. These boring questions matter more than the imported Italian tiles in the lobby.

Red Flags That Should Send You Running

Some warning signs are too big to ignore, no matter how attractive the price:

- Builder doesn't have clear RERA registration

- Vague answers about possession dates or construction progress

- Too-good-to-be-true pricing (there's always a catch)

- Aggressive pressure tactics ("This is the last unit at this price!")

- No existing projects to showcase (everyone starts somewhere, but it's riskier)

- Legal disputes around land ownership

- Unwillingness to show you the actual construction site

Trust your gut. If something feels off, it probably is. A good real estate consultant will encourage your skepticism, not dismiss it.

Making the Decision: When to Take the Leap

Here’s the truth: There’s no perfect time to buy a home. Interest rates will fluctuate. Prices will go up and down. The market will do its unpredictable dance.

But you should seriously consider buying when:

- You have job stability and consistent income

- You've saved at least 20-25% of the property cost

- You're planning to stay in the city for at least 5-7 years

- You've found a property that ticks most of your boxes (not all—perfection doesn't exist)

- The EMI + maintenance feels manageable, not suffocating

Your first home doesn’t have to be your forever home. It’s okay if it’s a stepping stone. What matters is that it’s a smart stepping stone that appreciates reasonably, serves your immediate needs, and doesn’t become a financial burden.

Disclaimer: The information provided in this blog is for general guidance only and should not be construed as professional advice. Property details, prices, and availability are subject to change. Readers are advised to verify all information independently and consult with financial and legal experts before making any purchase decisions. The projects mentioned are for reference purposes and details should be confirmed with the respective developers.